|

|

This site

is mobile

responsive

Discussions surrounding Malaysia’s rise as a global semiconductor powerhouse – which accounts for roughly 13% of global back-end chip testing and packaging, and over 7% of total global semiconductor trade – usually picture state-of-the-art factories, pristine cleanrooms, and the high-tech assembly lines of Penang, Kulim, or Johor. Yet behind every billion-ringgit semiconductor investment lies a foundational ecosystem that rarely makes the headlines.

To illustrate, the semiconductor value chain functions much like a large-scale theatrical production: The massive technology brands may get top billing, but their operations cannot succeed without the dedicated technical crew building the sets, maintaining the equipments, and keeping the running behind the scenes.

In the microchip world, this vital crew is represented by the Engineering Supporting Industries (ESI).

Amid today’s increasingly complex global supply chains, driven by geopolitical and technological shifts, this “hidden backbone”—comprising precision machining, automation support, and specialised maintenance—is transitioning from behind the scenes into the spotlight. It is no longer merely a support system; it has become one of Malaysia’s key competitive advantages.

Historically, developing nations attracted massive foreign investment (FI) primarily through conventional incentives: competitive real estate pricing, tax holidays, and low labour costs. The implicit promise to multinational anchor companies was: “Build your factory here, and the local supply chain will eventually catch up.”

Today, that investment playbook is no longer sufficient.

In an era of exponential demand for AI chips and automotive electronics, tech giants face compressed product lifecycles and stringent operational timelines. brutal time-to-market pressures and unforgiving structural bottlenecks. Consequently, multinational corporations can no longer afford long lead times for local supplier development.

As a result, investment decisions increasingly prioritise turnkey supply chain readiness. Global anchors favour economies with mature, pre-certified, and operationally integrated ecosystems that facilitate immediate integration from day one. In the absence of a comprehensive network of precision engineers, calibration experts, and toolmakers, capital will inevitably migrate to more prepared and ready countries.

Importantly, ESI is not a one-size-fits-all model; it is divided into back-end support (such as high-volume assembly, testing, packaging, jigs, and precision tooling) and front-end support (such as wafer fabrication equipment parts and high-tolerance machining). Each of these activities demands completely different technical specifications, strict quality standards, and distinct levels of supplier readiness.

Semiconductor fabrication is among the most complex, sophisticated, and capital-intensive processes globally. Under such unforgiving tolerances, a microscopic speck of dust or a machine part misaligned by a fraction of a millimetre can result in a catastrophic yield loss and severe financial deficits.

This highlights the critical role that ESI companies play as the technical foundation safeguarding operational uptime. Specifically, they provide:

The Bottom Line: Ultimately, ESI represents far more than capital expenses. It directly governs manufacturing throughput, yield optimisation, and overall cost efficiency.

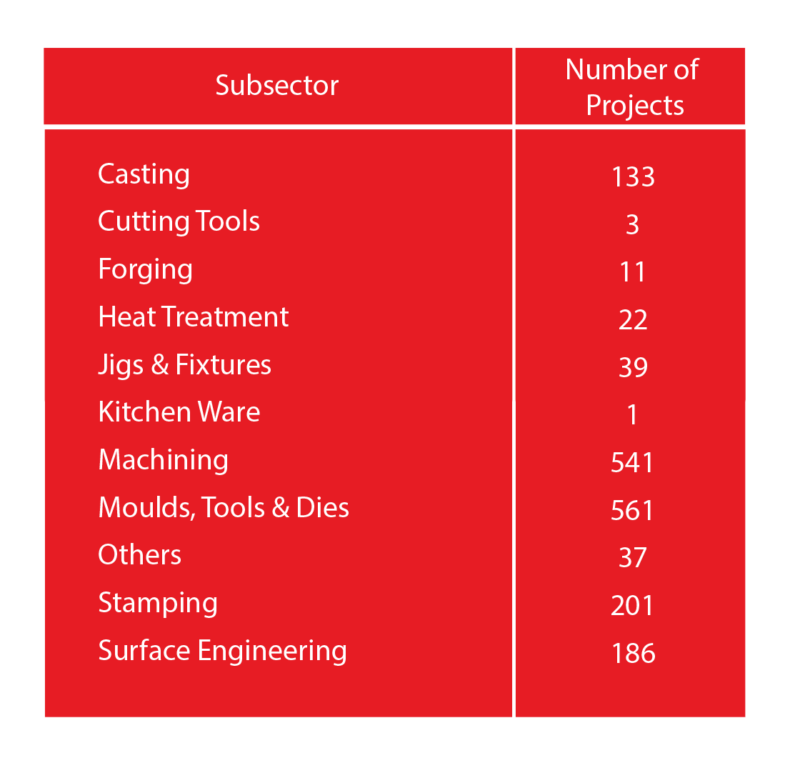

Far from being a nascent sector, Malaysia’s ESI ecosystem is exceptionally robust and far more mature than many realise.

MIDA’s records indicate that Malaysia is home to hundreds of engineering supporting firms, each operating within highly specialised technical subsectors:

These specialised operations underpin a broad range of industries, including semiconductors, aerospace, medical devices, automotive, and industrial automation. Many Malaysian companies today have successfully scaled into advanced capabilities such as:

Long-standing industrial clusters in Penang, Kulim in Kedah, Selangor, and Johor have fostered highly integrated supplier networks capable of supporting complex manufacturing ecosystems.

This deep-rooted industrial maturity continues to be one of the key factors behind Malaysia’s success in attracting high-profile semiconductor investments.

The global semiconductor landscape is undergoing a profound structural realignment. Spurred by supply chain lessons and an evolving trade landscape, global tech giants are aggressively diversifying their manufacturing bases through the “China+1” strategy. In evaluating alternative locations, global chipmakers increasingly choose Malaysia due to its distinct structural advantages. Decades of industrial clustering have given rise to a mature ecosystem boasting robust intellectual property (IP) protection, well-developed Free Industrial Zones (FIZs), a highly skilled, English-proficient engineering talent pool, and a seamless, facilitative regulatory framework. This positions the local ecosystem to seamlessly absorb high-value diversifications.

Expansion projects are taking place across Malaysia’s industrial hubs. From an operational standpoint, a robust local ESI network provides MNCs with transformative advantages, enabling them to:

By having and maintaining a reliable, highly responsive local engineering ecosystem, Malaysia transitions from being a temporary manufacturing pitstop into an indispensable, resilient global technology anchor.

However, unlocking the full potential of these opportunities requires addressing several challenges. If supply chain readiness represents the primary benchmark for attracting investment, Malaysia’s local small and medium enterprises (SMEs) must navigate specific structural headwinds to sustain the country’s competitiveness.

Elevating Malaysia’s ESI ecosystem demands deliberate, highly coordinated actions from the government and regulatory bodies, multinational corporations, and local firms. While initiatives such as supply chain programmes and strategic match-making platforms are a start, the industry needs to intensify its focus on a few critical levers:

National frameworks like the New Industrial Master Plan (NIMP 2030) and the National Semiconductor Strategy (NSS) serve as a strong foundation driving Malaysia’s ESI evolution. Rather than just offering passive roadmaps, these initiatives actively support rapid industrial upgrading, deeper supply chain integration, advanced technology adoption (such as Industry 4.0), and enhanced global competitiveness across the entire semiconductor ecosystem.

Malaysia’s engineering supporting industries are undergoing a profound structural evolution. They are evolving from basic back-office support into a core pillar of Malaysia’s high value industrial future.

Ultimately, Malaysia’s long-term competitiveness in the global semiconductor landscape won’t be determined by high-profile,multi-billion-ringgit production facility announcements—it will depend increasingly on the maturity, absolute readiness, and agility of the local engineering ecosystem that is working behind the scenes.

And as the global semiconductor race intensifies, these once-unsung heroes will pave our way into the global value chain. Ultimately, Malaysia’s ESI should no longer be viewed merely as auxiliary suppliers, but as strategic enablers of technological sovereignty, supply chain resilience, and long-term industrial competitiveness.

Explore other related content to further

explore MIDA’s insights.