Metal frame maker Econframe unfazed by recession fears, on the lookout for partnerships

22 Feb 2023

ECONFRAME Bhd, which debuted on the ACE Market of Bursa Malaysia in October 2020, is on the prowl for business partners that can help broaden its offerings.

“When the markets started to open last year, it was a good time for us to look into acquisitions. We are unfazed by [concerns of a] recession because the property upgrade market is ever present. Companies like Sime Darby [Property Bhd] and Mah Sing [Group Bhd] will continue to launch, and their sales figures are good,” Econframe managing director Lim Chin Horng tells The Edge.

The main businesses of Econframe, a metal door and window frame maker, involve the provision of total door system solutions; electronics and electrical systems and accessories; and solar energy products and systems. These are grouped into two segments — manufacturing and trading. According to the company’s 2022 annual report, the manufacturing segment contributed 84.3% and 83% to the group’s total revenue and profit respectively.

“Over these 22 years, we have built our brand by specialising in custom products to cater to our contractors’ needs. [Subsequently,] we started to bring in fire-rated doors [and] wooden doors, all of which are related products.

“We don’t want to go into general hardware products such as steel bars as we want to maintain our niche in custom products, which can also be used as value-added goods,” says Lim, who has experience in the manufacturing of dry cargo containers and mechanical metal parts. It was his observation of demand for metal door and window frames that led him to venture into the business in 2001.

Lim has a 21.39% stake in Econframe.

“As we have captured enough of [those] markets, it’s now time to grow. We have been so busy keeping up with demand that there is no time to sit,” he says. To this end, Econframe last month acquired a 65% stake in Lee & Yong Aluminium Sdn Bhd (LYASB), a manufacturer and installer of aluminium glazing, glass products and façade works such as aluminium windows and glass doors, for RM17.2 million.

This is the group’s first acquisition since its flotation exercise. Lim expects the deal, which is slated to be completed in the second half of this year, to contribute to an annual revenue of RM60 million to RM80 million in the next two years.

“We are targeting about RM90 million in revenue for the financial year ending Aug 31, 2023 (FY2023), with about 22% of the revenue coming from LYASB. They have the expertise and market,” Lim says of the deal.

He adds that since aluminium is required in windows and sliding doors, the addition of LYASB’s offerings to Econframe’s existing stable could more effectively tap the latter’s long-standing customers such as Mah Sing, IJM Corp Bhd and Sime Darby Property.

He says Econframe currently has 206 projects and an order book of about RM90 million, which is expected to last about 1½ years.

Lim declines to disclose Econframe’s market share but stresses that the company has capitalised on being a custom manufacturer.

It is noteworthy that shares in Econframe, which was trading at the 63 sen level last November, shot up to RM1.03 in the following month after Datuk Eddie Ong Choo Meng, 44, reportedly emerged as a minority shareholder in the company. Econframe’s 2022 annual report shows that as at Nov 25, 2022, Ong had a 2.11% stake in the company. Last Thursday, Econframe’s counter closed at 96 sen per share, valuing the group at RM304.89 million. Queried on the matter, Lim says he recently learnt that Ong, whom he knows as a friend, had emerged on the shareholder list.

“I believe Ong has exited the shareholder list. He probably came in for a short-term investment but there were no business deals that happened [between Ong and Econframe] during the period. We are always open to business opportunities and the chance to collaborate, but we did not have any specific conversations about this matter,” Lim says.

Ong, who frequently made the news as he expanded his business stable by buying equity interest in public-listed entities through his family vehicles, Hextar Holdings Sdn Bhd and Hextar Rubber Sdn Bhd, controls nine listed companies on the bourse.

Expansion strategy

Currently, Econframe makes about 35,000 door frames a month. It is focused on the Klang Valley, which comprises 75% of its orders, with the remaining 25% coming from Seremban, Negeri Sembilan; Melaka; and Sabah and Sarawak.

“As we are comfortable with [the quantum of] our existing orders and utilisation of capacity, we are careful not to ‘over-expand’ or become ‘overly diversified’. That could put us at risk of bad debts or [needing to accept] ‘contra properties’.

“Therefore, we would rather tap our existing customer base and give them new products, [hence our search for partners with offerings that add value to ours]. Neither will we venture into export markets for now so that we can maintain our focus on Malaysia, which alone has kept us very busy,” Lim says.

As part of the group’s expansion plans for its manufacturing operations, Econframe acquired a parcel of industrial property for RM8.13 million from JC Senco Realty Sdn Bhd (formerly JC Jaya Realty Sdn Bhd).

Econframe said the property, which has a gross built-up area of more than 35,000 sq ft near the group’s existing facilities, will be enough for the group to expand its manufacturing activities and improve its manufacturing workflow and efficiency.

The group says it will also upgrade its manufacturing technology and processes via automation and adopting advanced robotic technology, following the completion of the acquisition of the property.

The group also expects automation to improve the operational efficiency, safety and capacity, contributing positively to the group’s earnings for the next financial year.

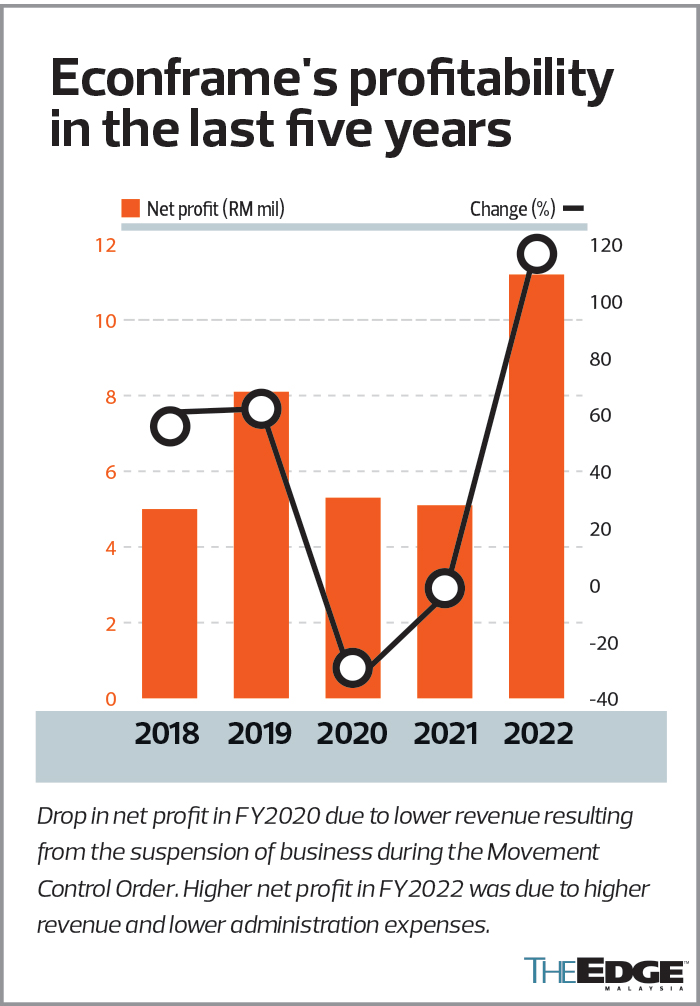

Econframe’s net profit for the first quarter ended Nov 30, 2022 (1QFY2023), dipped 1.5% to RM2.3 million from RM2.7 million the year before. Revenue was RM16.9 million, rising 27% year on year from RM13.3 million.

In an exchange filing, the group attributed the decrease in profit to the hike in cost of sales as a result of the increase in raw material cost and higher operational costs.

This is evidenced by the compression in its gross profit and operating profit margins during the quarter compared with a year ago. It recorded a gross profit margin of 27.8% in 1QFY2023 compared with 35.34% in 1QFY2022, while operating profit margin fell to 18.75% in 1QFY2023 from 26.63% a year ago.

Meanwhile, it said the increase in revenue in 1QFY2023 was contributed by the manufacturing segment, driven by higher sales orders for metal door frames during the period.

The improved business performance saw its net cash flow generated from operating activities increase to RM784,000 for the quarter under review compared with RM153,000 a year ago. As at Nov 30, 2022, Econframe had net cash of RM26.2 million, which should give it headroom to gear up for expansion.

Although it is in net cash position, Econframe has been conservative in its dividend payout and does not have a formal dividend policy. It paid out a first interim single-tier dividend of 0.5 sen per ordinary share, amounting to a total dividend of RM1.625 million for FY2022, representing a dividend payout of 14.5% of the net profit attributable to owners of the company for the period. In FY2021, it did not pay any dividends to shareholders.

As to how Econframe will maintain its margins in an environment of rising material prices, Lim explains that the “prices of raw materials are locked in with suppliers as soon as the orders come in” and increased costs are then passed on to customers.

“Thanks to the nature of our business of custom products, our clients understand that the orders are based on prevailing input costs, which sometimes result in higher selling prices. They get this. As for Econframe, we command a reasonable margin for our products. I wouldn’t say it is very high, but it is reasonable,” Lim says, adding that Econframe has an existing base of about 800 business-to-business clients.

Source: The Edge Markets

{kind=link}